After the IMF Director Kristalina Georgieva had already pointed out the inadequacies of the Common Framework of the G20 for the restructuring of sovereign debt in clear words in December, the World Bank is now following suit. In the Global Economic Prospects published on 11 January, the authors dedicate a separate chapter to the current debt situation, in which they compare the measures taken by the G20 so far with past debt restructuring and debt relief initiatives.

The core message is clear: many countries find themselves in a highly critical debt situation and urgently need real debt relief. However, the G20 Common Framework is not suitable for granting efficient and sustainable debt relief. In its current form, it resembles the unsustainable debt restructuring measures of the early 1980s. Insufficient debt relief led to a “lost development decade” in many countries of the Global South.

LESSONS OF THE PAST

The World Bank’s evaluation of past debt relief initiatives can be summarised in four points:

- Comprehensive debt relief has in the past almost always been granted as part of a coordinated initiative.

- In the past, debt relief came too late and was only granted after the crisis had dragged on for Among other things, this was due to overly optimistic debt sustainability analyses and the refusal of creditors to recognise that many countries were not only in a short-term liquidity crisis, but had a long-term solvency problem and therefore needed real relief. In contrast, studies showed that early debt restructurings with sufficient haircuts would be beneficial for all involved.

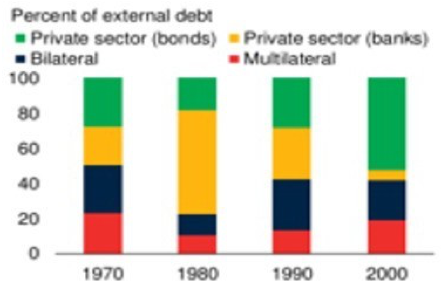

Fig. 1: Composition of claims by creditor in Brady countries Source: World Bank (2022): Global Economic Prospects – Special Focus: Resolving High Debt after the Pandemic. Note: Extensive lending by private creditors in the 1970s drove many countries into over-indebtedness and resulted in a good 80 percent of claims on Brady countries being held by private creditors at the beginning of the crisis in 1980. By 1990, when private creditors were finally comprehensively involved in debt restructuring, many private creditors had already successfully withdrawn. - Private creditors have not been sufficiently involved in debt relief in the past. Even in the context of the HIPC and MDR initiatives, the prescribed equal treatment, according to which private creditors should grant at least as much debt relief as was granted by public creditors, could not be successfully enforced. The most comprehensive participation of private creditors was in the Brady initiative after 1989. Private claims were reduced by approx. 37 percent. At the time, this was only possible through coordinated action by multilateral creditors and the governments of the countries of the Global North in which the private creditors were based. Among other things, the IMF introduced its so-called Lending into Arrears Policy for the first time, which strengthened the negotiating power of debtors vis-à- vis uncooperative creditors. However, the Brady debt restructurings also took place only after almost a decade of inadequate debt relief operations and public loans had led to a large part of the previously private claims being transferred to public creditors (cf. Fig. 1).

- Truly comprehensive debt relief under the HIPC and MDR initiatives could be granted, among other things, by also writing off multilateral claims.

THE CURRENT SITUATION

The pandemic-induced recession met an already critical debt situation in many low- and middle-income countries and has further fuelled indebtedness. For a sustainable economic recovery, many countries will need comprehensive debt relief. According to the World Bank paper, providing this in sufficient volume and in a timely manner is complicated by four developments that complicate the creditor structure:

- Due to the large share of private (bond) claims on low-income countries compared to the 1980ies. It must be assumed that around 50 percent of the outstanding bonds do not contain collective action clauses, which are supposed to facilitate an orderly debt restructuring with bondholders. In addition, it can be observed that private creditors are becoming increasingly litigious and suing their public debtors in national courts for repayment.

- By the weight of public bilateral creditors outside the Paris Club, including in particular China and the Gulf states.

- Due to the share of non-classical debt instruments such as the agreement of currency swaps.

- By blurring the distinction between public and private creditor institutions, as in the case of the China Development Bank (CDB) or the German Kreditanstalt für Wiederaufbau (KfW).

SHORTCOMINGS OF THE COMMON FRAMEWORK

The Common Framework is a welcome, necessary first step in creditor coordination, without which an orderly exit from over-indebtedness is not possible, says the World Bank. In its current form, however, the Common Framework is not suitable for ensuring sufficient debt relief and a fair distribution of costs between the various creditors. In particular, it is problematic that public creditors, as in the early 1980s, rely on combating debt crises primarily through payment extensions and insufficient debt service relief. Ambitious relief is urgently needed for many countries. Furthermore, the Common Framework lacks clear principles on how private creditors can be involved in debt relief.

WHAT TO DO NOW

In order to increase the effectiveness of the Common Framework, it would first be necessary to commit to actually granting comprehensive debt relief where the debt situation is unsustainable. The binding participation of private creditors could be achieved, among other things, through national legislation. Debtor countries should be granted a moratorium during the negotiations and time limits for the negotiation process would be helpful to make the negotiations more efficient.

Ultimately, the authors of the World Bank publication propose to expand the international debt architecture through a mechanism that would make debt restructuring agreements binding on all creditors by majority vote. What exactly is meant here, however, remains up in the air. They speak of aggregated collective action clauses, through which a majority decision would also be binding on claims that are already outstanding. However, the very nature of collective action clauses is that they are a contractual element in the agreement of credit agreements and therefore cannot be effective retrospectively for claims that are already outstanding. A majority decision binding on all creditors and all credit instruments, on the other hand, could become effective through a reform of international negotiation structures – such as the SDRM proposed by the IMF in 2001. Although the objective of the newly proposed “mechanism” (binding for all creditors and all already outstanding claims) therefore rather relates to a structural reform of international negotiation formats, this is called for under the guise of Collective Action Clauses, i.e. contractual reforms. The question is whether there is disagreement within the World Bank on how openly to move away from the previously defended position that contractual changes alone are sufficient.

The positioning regarding MDB participation in debt restructuring, which has been vehemently excluded by the World Bank so far, also remains open. In the analysis of past debt relief measures, the participation of multilateral creditors is emphasised as a success factor. In the current situation, the authors of the analysed paper speak of the need for all public and private creditors to participate. An exception for multilateral claims is not explicitly called for. However, there is no statement that the World Bank itself is prepared to reduce part of its claims within multilateral debt relief frameworks.

Decisive for the further treatment of the Common Framework will ultimately be whether this analysis is followed by action and concrete reforms are taken. After all, the need for this has been said often enough – now also by the World Bank.